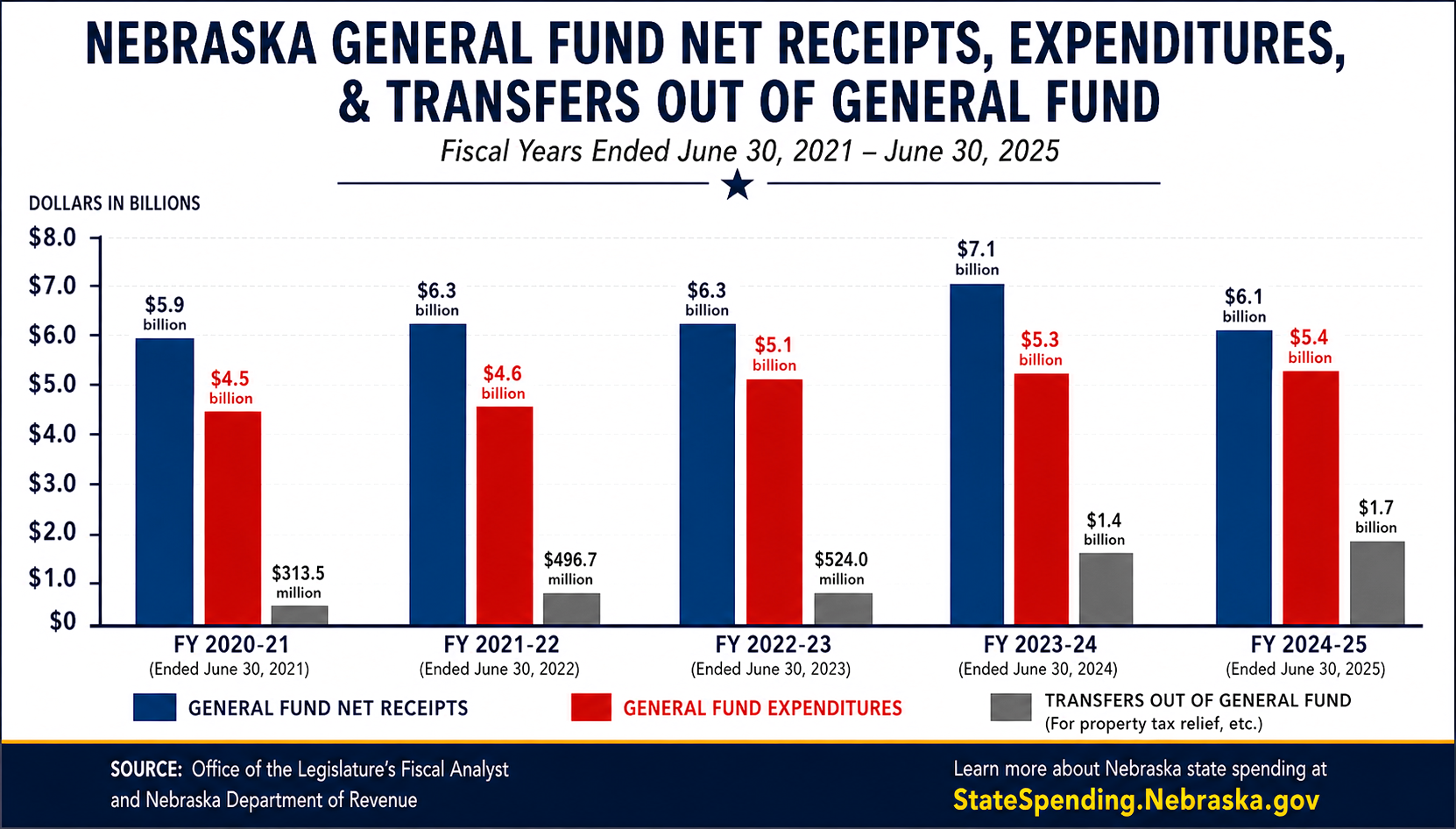

Nebraska’s General Fund is the state government’s primary spending account, funded largely by sales & income taxes. Here’s a look at recent General Fund expenditures and receipts, as well as transfers out of the General Fund (primarily to offset property taxes collected by local government, including K-12 school districts). These transfers have occurred mostly to pay for the State’s:

- School Property Tax Relief Fund ($750M in 2025) to provide property tax credits for K-12 school taxes;

- Property Tax Credit Fund ($395M in 2025) to provide credits on property owners’ tax statements from local government;

- Education Future Fund ($250M in 2025) to provide K-12 special education and foundation aid; and

- Community College Future Fund ($253.3M in 2025) to provide community college funding.

COMPARISON: In FY 2019-20, the State's property tax relief programs (Property Tax Credit, Personal Property Tax Exemption, and Homestead Exemption) totaled approximately $381.1 million.

Five years later, in FY 2024-25, the State's property tax relief programs (listed above, plus $149 million for the Homestead Exemption) totaled roughly $1.8 billion.